Asset Allocation is the Key

At the heart of the Assetfirst Service sits a range of risk-graded model portfolios which have been developed using proprietary research across the full universe of asset classes. Central to the construction of the portfolios is our belief that asset allocation - not security selection - is the key driver of portfolio returns. To precisely fulfil our asset allocation requirements at the lowest possible cost, where possible, we use Exchange Traded Funds (ETF) and Index Tracking Funds. Our Balanced Portfolio, which has exposure to 15 sub asset classes has a TER of just 0.41%...

Tactical Asset Allocation

Click for a larger version of the example

Example Holdings within the Assetfirst Balanced Portfolio

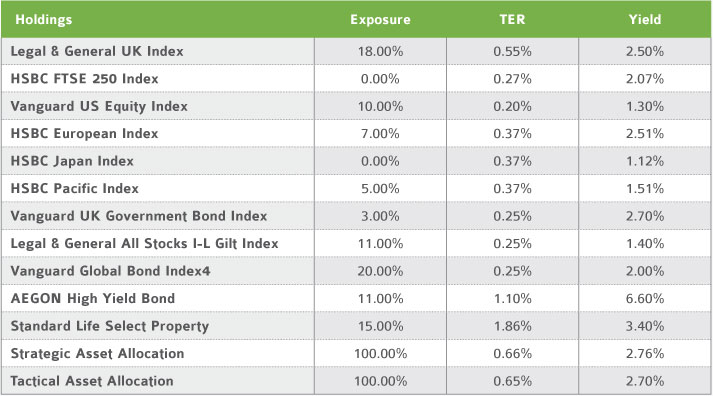

For smaller portfolios or where regular premiums are being paid we realise that the dealing costs associated with ETF investment may be an issue. In addition to this certain investment platforms do not allow access to ETFs. For these reasons the Assetfirst service includes a mirror range of portfolios which utilise traditional index tracking funds instead.

Click for a larger version of the example

Example Holdings within the Assetfirst Balanced LITE Portfolio

Click for a larger version of the example

Six Step Process

Assetfirst has developed its own proprietary Strategic Asset Allocation (SAA) methodology following a rigorous, six-step process and forms the bedrock of a top-down investment management programme.

Risk Budget

Our process begins by identifying an appropriate risk budget - a ceiling for exposure to ‘risky’ assets - for the median risk SAA in a series of templates. The solution to this problem will have a fundamental influence on the resulting range of SAA templates, forming the pivot upon which both lower and higher risk templates will hinge.

Opportunity Set

The opportunity set defines the spectrum of asset classes and sub-classes that will be included as a matter of course in the SAA. The asset classes that make up the opportunity set may include domestic and international equities & bonds, real estate, commodities, hedge fund schemes.

Risk-Return Vector

The description of the risk-return vector is dependent upon the chosen method of identifying an individual investor’s ‘attitude to risk’ – usually in the form of a risk questionnaire. Broadly speaking the risk-return vector is the distance between SAA with the lowest risk on one hand and the highest risk on the other as well as the angle at which risk increases.

Doctrinal Set

The doctrinal set is concerned with the intended method of managing the mix of assets over time. Will the SAA be frequently or infrequently re-balanced, whether some form of active asset mix management will be employed?

Mean-Variance Optimisation

We employ a mean-variance optimisation (MVO) technique to identify the appropriate range of SAA templates. The generalised MVO method has the advantage of being widely described in financial texts and research publications. Harry Markowitz, the architect of Modern Portfolio Theory, reduced the optimisation problem to that of finding mean-variance efficient portfolios. Efficient portfolios have the highest expected return (the ‘mean’) for a given level of risk (the ‘variance’) or the lowest risk for a given level of expected return.

Stress Tests

The solution to the MVO problem is dependent on a large number of assumptions (close to 400 in some cases), including estimates of prospective risk, return and paired correlation coefficients for each asset and sub-asset class. The uncertain nature of these assumptions is a source of weakness which we try to limit by applying both forward and backward-looking stress tests to the full range of SAA templates. This provides a wealth of data to support adviser and investor understanding, particularly of the risks associated with investment.

Passive investment specialist IFA Andrew Whiteley and Independent Analyst Steve Williams have joined forces to launch assetfirst, a unique, fee-based, model portfolio service designed to assist other advisers to comply with the demands of the Retail Distribution Review (RDR)...

Passive investment specialist IFA Andrew Whiteley and Independent Analyst Steve Williams have joined forces to launch assetfirst, a unique, fee-based, model portfolio service designed to assist other advisers to comply with the demands of the Retail Distribution Review (RDR)...